Clearlake Chelsea Exposure Research 6 May 2026

Prepared as of 6 May 2026. Currency: figures cited in £ unless stated. Where SEC schedules report in USD, the original disclosure is preserved.

- Clearlake Capital Group, L.P. controls approximately 61.5–61.85% of the Chelsea FC ownership group through Blues Investment Midco LP (a Cayman-incorporated limited partnership), and by 30 June 2025 the group’s ultimate parent (22 Holdco Limited) had received approximately £1.794 billion of capital attributable to Clearlake out of £2.9 billion in total consortium equity, making this the firm’s single largest sports-and-media position and its largest disclosed equity ticket in any single asset.

- In addition to its equity, Clearlake holds direct lending exposure to the deal architecture through Clearlake Opportunities Partners III (COP III, $2.5bn special-situations fund closed Sept 2022), which provided a mezzanine/PIK credit facility to Blues Investment Midco LP to finance Clearlake’s equity contribution.

- The exact principal of this Cayman-level facility is not disclosed in UK Companies House filings but is consistent with an estimated £300–450 million range based on third-party institutional disclosures and Clearlake’s own statement that “COP III led the Chelsea Football Club investment on behalf of Clearlake’s affiliated funds and other partners.”

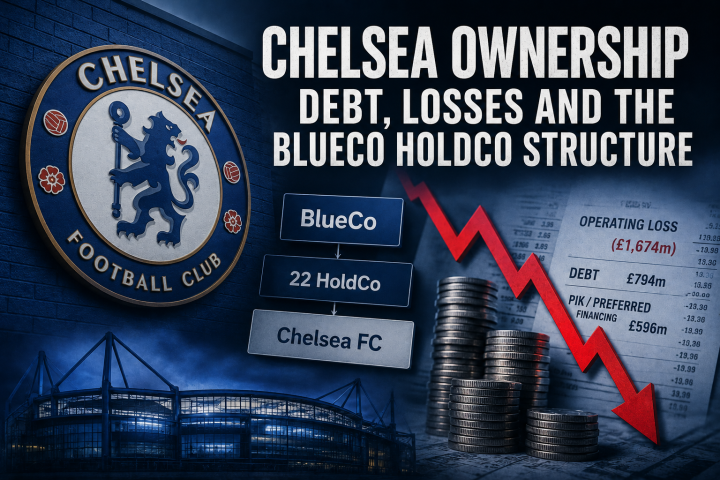

- The senior bank debt at BlueCo 22 Limited (£794.2m at 30 June 2025, originated 12 July 2022, maturing 13 July 2027) and the £595.9m PIK / preferred-equity-style loan at 22 Holdco Limited (originated September 2023, maturing August 2033) are NOT held by Clearlake, they are provided by JPMorgan/Bank of America (senior) and Ares Management (PIK), respectively. Clearlake’s exposure is therefore primarily equity at the UK level, with its own credit fund providing leverage one tier above (at the Cayman Midco) where it is invisible to UK Companies House but visible through Clearlake’s own marketing materials and PA PSERS disclosures.

The widely cited debt facilities at Chelsea (£794.2m senior at BlueCo 22; £595.9m PIK at 22 Holdco) are third-party. Clearlake is not the lender to either UK entity.

UK Companies House charge filings (charge 139495520001 registered 12 July 2022 against BlueCo 22; charge 140755180001 registered 22 August 2023 against 22 Holdco) name third-party lenders, not Clearlake funds.

Clearlake’s direct exposure to Blueco 22 Limited and 22 Holdco Limited is held in the form of A Ordinary shares of 22 Holdco Limited (the ultimate UK parent), held through Blues Investment Midco LP (Cayman LP, controlled by Clearlake).

Clearlake’s equity is held in the Cayman Islands via Blues Investment Midco LP

- Blues Investment Midco LP; Cayman Islands limited partnership; the registered shareholder of 61.85% of 22 Holdco Limited’s A Ordinary shares; was the original PSC of 22 Holdco Limited until the PSC register was updated on 30 June 2023, replacing it with the natural-person PSCs Behdad Eghbali and José E. Feliciano (Clearlake co-founders).

- The Boehly side is held through Blueco 22 Holdings L.P. (UK-registered limited partnership LP022606, registered 23 May 2022), of which Todd Boehly is sole general partner.

Clearlake’s 22 Holdco equity contributions to date (May 2022 – June 2025)

Per the 22 Holdco Limited consolidated accounts for the year ended 30 June 2025:

| Date | Event | Total consortium equity in 22 Holdco | Clearlake share | Boehly side share |

| 30 May 2022 | Acquisition completion (£2.5bn purchase price + £1.75bn commitment; equity contribution to UK group) | Initial Ordinary A/B share capital subscribed via 22 Holdco; nominal £25,499.80; majority of equity injected as share premium | 61.85% (Ordinary A) | 38.15% (Ordinary B) |

| Year ended 30 June 2024 | Various tranches | c. £2.45bn cumulative | c. £1.51bn | c. £0.94bn |

| Sept – Oct 2024 | 19 million new shares issued; £190m raised | +£190m to c. £2.64bn | +£117m | +£73m; Clearlake stake nudged from 61.5% to 61.85%, Boehly group from 38.5% to 38.15% per Cordell analysis |

| 8 Oct 2024, 19 Nov 2024, 27 Feb 2025, 25 Mar 2025 | Five staged SH01 allotments at BlueCo 22 (mirrored at 22 Holdco) | Nominal share capital at BlueCo 22 grew from £1,100 to £6,100 | Clearlake A Ordinary line | Boehly B Ordinary line |

| Year ended 30 June 2025 | 179.4m A Ordinary + 110.6m B Ordinary issued, raising £450m total in fresh equity (almost entirely as share premium) at 22 Holdco level | +£450m → c. £2.9bn cumulative | +£278m (Clearlake A) | +£172m (Boehly B) |

| Cumulative at 30 June 2025 | £2.9bn total consortium equity in 22 Holdco | £1.794bn (Clearlake) | £1.106bn (Boehly group) |

Source: 22 Holdco Limited consolidated accounts year ended 30 June 2025 (filed 12 April 2026, 52 pages);

The £450m raised during 2024/25 is the largest single equity round since the original acquisition. Of that, c.£330m was on-lent down to Chelsea FC Holdings Limited; the £120m balance remained at the parent level.

Clearlake’s £1.794bn equity contribution: fund attribution

Clearlake’s own press release on COP III’s final close (20 September 2022) is the single most authoritative attribution statement in the public domain:

“COP III has already led investments in AMCS … and Chelsea Football Club… COP III led the Chelsea Football Club investment on behalf of Clearlake’s affiliated funds and other partners.” Clearlake Capital, 20 Sept 2022

This makes clear that Chelsea is NOT sitting in flagship Clearlake Capital Partners VII alone, despite some early Markets Group reporting suggesting Fund VII held the position. Rather, the equity ticket is split across:

| Clearlake Vehicle | Type | Size at close | Role in Chelsea |

| Clearlake Opportunities Partners III (COP III) | Special-situations / opportunistic credit & equity hybrid (Delaware LP) | $2.5bn (final close 20 Sept 2022; oversubscribed vs $1.5bn target) | Lead investor of record for the Chelsea position; provided both equity and the Midco credit facility (see §5) |

| Clearlake Capital Partners VII (Fund VII) | Buyout flagship (Delaware LP) | $14.1bn (final close 18 May 2022, just twelve days before Chelsea acquisition completion) | Co-investor; reported by Markets Group / Pensions & Investments to hold a tranche of the Chelsea equity, although Clearlake has not separately confirmed Fund VII’s specific Chelsea allocation |

| Co-investment vehicles / continuation funds / SMAs | Various | Part of “more than $25bn raised since January 2021, including … continuation and co-investment funds” (Clearlake, Sept 2022) | Held alongside COP III and Fund VII to absorb the unusually large ticket size; specific named co-invest vehicles are not publicly disclosed |

| WhiteStar Asset Management / Clearlake Credit (incl. MV Credit, acquired Sept 2024) | Credit / CLO platform | – | No disclosed direct exposure to Chelsea group entities; included for completeness |

The exact dollar split between COP III, Fund VII and co-investors is a private matter between Clearlake and its LPs and has not been publicly disclosed. Bloomberg (April 2026) and other reporting confirms Clearlake’s investors view Chelsea as a Clearlake position rather than a Fund VII only position; PSERS-level disclosure consistently lists the exposure under COP III.

COP III / Blues Investment Midco LP credit facility; Clearlake’s only direct lending exposure

This is the single most important Clearlake-as-lender exposure to the Chelsea structure. Because Blues Investment Midco LP is a Cayman Islands entity, it does not file accounts at UK Companies House; the loan therefore does not appear in BlueCo 22 or 22 Holdco UK statutory filings.

| Parameter | Detail | Source |

| Lender | Clearlake Opportunities Partners III (COP III) | Clearlake press release 20 Sept 2022; PSERS investment narrative; theesk.org analysis 2 May 2026 |

| Borrower | Blues Investment Midco LP (Cayman LP, Clearlake-controlled) | UK Companies House PSC history of 22 Holdco (Blues Investment Midco Limited / LP listed as PSC until 30 June 2023) |

| Purpose | Finance Clearlake’s £1.5–1.8bn cumulative equity contribution into 22 Holdco; “upper-tier” leverage above the UK group | Clearlake / theesk.org reconstruction |

| Estimated principal | £300m – £450m (working estimate; not publicly disclosed) | Reconstruction by theesk.org from PSERS disclosure reports and group financial architecture |

| Estimated coupon | 12.5%–15.0% all-in yield; SONIA + 8.5–10.0% equivalent | Market convention for 2022–2024 mezzanine; PSERS COP III performance data |

| Structure | Mezzanine PIK notes (interest capitalised, not paid in cash) | Standard COP III mandate; aligned with 22 Holdco PIK |

| Maturity | 203 –2033 (aligned with 22 Holdco PIK) | Reconstruction; not separately disclosed |

| Security | Pledge over 179.4m + Ordinary A shares of 22 Holdco Limited (held by Blues Investment Midco LP) | Standard for facilities of this kind |

| Subordination | Subordinated to all UK group debt (BlueCo 22 senior; 22 Holdco PIK); senior to common equity held by Clearlake LPs | Structurally implicit |

The principal, exact pricing, exact maturity and warrant/equity-kicker terms of the COP III–Midco facility are NOT in the public record. The numbers above are best-available reconstructions from third-party analyses and PSERS public investment-monitoring documents. They should be cited as estimates, not as audited disclosures.

Clearlake has provided no third-party guarantees, warrants or derivatives that are publicly disclosed

A search of Companies House charges for BlueCo 22 Limited (13949552), 22 Holdco Limited (14075518), BlueCo 22 Midco Limited (14213798), BlueCo 22 Properties Limited (14304080) and Chelsea FC Holdings Limited (02536231) does not reveal any registered charge in favour of any Clearlake fund, vehicle, or affiliate.

Equally, no SEC-registered Clearlake vehicle has filed schedule-of-investments line items disclosing a direct loan or warrant to BlueCo 22 Limited or 22 Holdco Limited (the SEC schedules that do list “22 HoldCo Limited”, ARCC, ASIF, CADC, are Ares vehicles, not Clearlake).

Clearlake’s only structured exposure where warrants or equity kickers are conceivable is the COP III Midco loan, which by its nature in a special-situations fund is highly likely to contain equity-like features; however, none has been independently verified in public filings.

Other corporate-structure entities and Clearlake’s relationship to each

| UK / Offshore entity | Companies House / registry no. | Role | Clearlake direct exposure? |

| 22 Holdco Limited (formerly Blues Partners Limited) | 14075518 (England) | Ultimate UK parent; counterparty to the Ares £595.9m PIK | Yes: equity (61.85% A Ordinary via Blues Investment Midco LP) |

| BlueCo 22 Limited | 13949552 (England) | UK intermediate holding; counterparty to the £794.2m senior bank facility (charge 12 July 2022) | Indirect equity only (wholly-owned by 22 Holdco) |

| BlueCo 22 Midco Limited | 14213798 (England) | Football-asset midco (holds Chelsea FC Holdings, Chelsea Women, Strasbourg) | Indirect equity only |

| BlueCo 22 Properties Limited | 14304080 (England) | Holds the Stamford Bridge hotels and car parks (£76.5m intra-group sale 2022/23) | Indirect equity only |

| Chelsea FC Holdings Limited (formerly Chelsea Village PLC / Chelsea FC PLC) | 02536231 (England) | Operating subsidiary; received £315m of new shares in 2023/24 + c. £330m of the £450m raised in 2024/25 | Indirect equity only |

| Chelsea Football Club Women Ltd | 07377729 (England) | Owned 92% by BlueCo 22 Midco (8% sold to Seven Seven Six / Alexis Ohanian May 2025 at $265.2m valuation, Giannis Antetokounmpo joined 2026) | Indirect equity only |

| BlueCo 22 Investor Holdings Limited | 14075320 (England, dissolved 18 July 2023) | Defunct holding entity used in the original deal architecture | Historical only |

| BlueCo 22 Holdings L.P. (Boehly side) | LP022606 (England, registered 23 May 2022) | Boehly group’s holding LP; sole GP is Todd Boehly | None; this is the Boehly LP, not the Clearlake LP |

| Blues Investment Midco LP (Clearlake side) | Cayman Islands LP | Clearlake’s direct holding LP, owns 61.85% of 22 Holdco Limited | Yes: equity holder; receives the COP III mezzanine facility |

There is no listed entity in Delaware or Luxembourg in the publicly visible Chelsea ownership chain (although Clearlake’s own funds COP III, Fund VII, Fund VIII are Delaware/Cayman/Luxembourg structures).

Details

Acquisition financial structure (May 2022)

- Total transaction: £4.25 billion ($5.3 billion) approved by HM Government 25 May 2022; closed 30 May 2022.

- £2.5 billion to acquire Chelsea share capital (paid into a frozen account intended for Ukraine war victims).

- £1.75 billion 10-year commitment to invest in stadium, academy, women’s team and Chelsea Foundation (commitment, not at-completion cash).

- £49.8 million paid to former Chelsea directors.

- Acquisition equity injected through 22 Holdco Limited (UK), funded principally by Clearlake (61.85%) and the Boehly group (38.15%, comprising Boehly’s vehicles, Mark Walter c. 13%, Hansjörg Wyss).

- Equity at completion was raised entirely by the consortium, there was no acquisition-financing debt at the BlueCo 22 / 22 Holdco level on Day 1; the senior facility (BlueCo 22 charge dated 12 July 2022) post-dates close by c. 6 weeks.

- Acquirer financial advisors: Deutsche Bank, Goldman Sachs, Moelis & Co., Robey Warshaw. Legal: Latham & Watkins, Paul Weiss, Sidley Austin.

Senior facility at BlueCo 22 Limited (NOT a Clearlake position)

- Original size: $957m equivalent (c. £780m), comprising c. $359m revolving credit + c. $598m term loan; arranged by JPMorgan and Bank of America.

- Charge registered 12 July 2022 (charge 139495520001).

- Pricing: SONIA + 3.25%; effective 7.5–8.0% during 2024/25.

- Outstanding 30 June 2024: c. £755.2m.

- Outstanding 30 June 2025: £794.2m.

- Maturity: 13 July 2027 (refinancing wall).

- Cash-pay, not PIK.

- Secured by floating charge over BlueCo 22 group assets including the shares of Chelsea FC Holdings Ltd and RC Strasbourg.

- Lenders disclosed in 22 Holdco accounts as “BlueCo Term Loans”; specific syndicate not publicly itemised.

- No Clearlake fund is among the disclosed lenders.

PIK / “preferred equity” facility at 22 Holdco Limited (NOT a Clearlake position)

- Lender of record: Ares Management Corporation, originating through Ares Capital Management LLC’s Opportunistic Credit / Sports, Media & Entertainment desk.

- Originated September 2023; charge registered 22 August 2023 (charge 140755180001).

- Original principal: £410.2m ( approx $500m).

- Outstanding 30 June 2025: £595.9m (growth of £185.7m purely from PIK accrual + possible delayed-draw activity).

- Coupon: SONIA + 7.50% PIK floating; SEC schedules (Ares Capital Corp Form 10-K FY2024; Ares Strategic Income Fund 10-Q FY2023; Form 424B3 FY2024) show specific tranches at 12.46%, 12.63%, 12.73%, and 12.96% PIK with $11.5–57.9m principal-equivalent line items.

- Syndicated internally across Ares Capital Corporation (ARCC, NASDAQ-listed BDC), Ares Strategic Income Fund (ASIF), and CION Ares Diversified Credit Fund (CADC), disclosed to the SEC under the Sports, Media & Entertainment industry classification.

- Maturity: 22 August 2033.

- Includes a delayed-draw/evolving commitment of approximately $14.0m (per ARCC disclosures), undrawn at most recent reporting.

- Likely embedded warrants / equity-kicker/convertible terms (Ares’ Opportunistic Credit standard structure), not separately disclosed in the public domain.

- No Clearlake fund participates as lender. This is an Ares position, syndicated to Ares-managed vehicles only.

COP III credit facility to Blues Investment Midco LP, the Clearlake lending exposure

This is the only credit-side exposure of any Clearlake fund to the Chelsea ownership architecture. Per Clearlake’s own press release of 20 September 2022 (“COP III led the Chelsea Football Club investment on behalf of Clearlake’s affiliated funds and other partners”), and per PA PSERS’ public allocation reporting for COP III (PA PSERS is a disclosed LP in COP III), the structure is:

- COP III (Clearlake special-situations fund, $2.5bn closed 20 Sept 2022, Delaware LP, Paul Weiss legal counsel, Credit Suisse placement agent) provided a mezzanine PIK loan to Blues Investment Midco LP, the Cayman LP that holds Clearlake’s 61.85% stake in 22 Holdco Limited.

- Loan proceeds were used to fund Clearlake’s equity contribution into 22 Holdco (i.e. it is “fund-level leverage” or “back-leverage”, not company-level leverage).

- Estimated economics: principal £300–450m; pricing SONIA + 8.5–10.0% (mid-teen all-in yield); structure PIK; maturity 2030–2033.

- Security: pledge over Clearlake’s A Ordinary shares in 22 Holdco Limited.

- Not disclosed in UK Companies House (Cayman counterparty; outside UK charge regime).

- Not disclosed in any SEC schedule (COP III is a private fund and does not file public schedules).

The function of this back-leverage facility is twofold: (i) it enhances Clearlake’s IRR on the deal by reducing the equity check from the GP and Fund VII/co-investors, and (ii) it provides PSERS and other COP III LPs with a high-yielding, credit-like exposure to the Chelsea asset that complements the equity exposure held in Fund VII / co-investment vehicles. Bloomberg and Taipei Times (April 2026) reporting on Clearlake’s Fund VIII fundraising difficulties references the firm doubling its own GP commitment to Fund VIII to c. $600m. Fund VIII is a separate vehicle and as of May 2026 has no disclosed direct Chelsea exposure.

Timeline of all Clearlake-relevant events, May 2022 – May 2026

| Date | Event |

| 2 March 2022 | BlueCo 22 Limited incorporated (Companies House 13949552) |

| 28 April 2022 | “Blues Partners Limited” (later 22 Holdco Limited) incorporated (14075518) |

| 18 May 2022 | Clearlake Capital Partners VII final close at $14.1bn |

| 23 May 2022 | BlueCo 22 Holdings L.P. registered (LP022606), Boehly side holding LP |

| 25 May 2022 | UK government approves £4.25bn acquisition |

| 30 May 2022 | Acquisition completes; equity injected from Blues Investment Midco LP (Cayman) and BlueCo 22 Holdings L.P. |

| 4 July 2022 | BlueCo 22 Midco Limited incorporated (14213798) |

| 12 July 2022 | Charge 139495520001 registered against BlueCo 22 Limited ;original c. $957m JPMorgan/BofA senior facility |

| 18 August 2022 | BlueCo 22 Properties Limited incorporated (14304080) |

| 20 September 2022 | COP III final close at $2.5bn announced; press release confirms COP III “led the Chelsea Football Club investment on behalf of Clearlake’s affiliated funds and other partners” |

| 22 June 2023 | Acquisition of RC Strasbourg Alsace (€75m, c. 99.97% via BlueCo Alsace) |

| 30 June 2023 | 22 Holdco PSC register updated: PSC changed from “Blues Investment Midco Limited” to natural persons Eghbali, Feliciano (and Boehly disclosed as director/holder) |

| 18 July 2023 | BlueCo 22 Investor Holdings Limited (14075320) dissolved |

| 22 August 2023 | “Blues Partners Limited” renamed 22 Holdco Limited; Ares £410.2m PIK loan charge registered (140755180001) |

| FY2023/24 | Chelsea FC Holdings issues £315m of new shares to BlueCo 22 group (intra-group on-lent equity); £198.7m intra-group “sale” of Chelsea Women to BlueCo 22 Midco for PSR purposes (Premier League review pending) |

| 8 Oct 2024 | First of five 2024/25 SH01 allotments at BlueCo 22 (£1,100 → £3,100 nominal) |

| Sept – Oct 2024 | 19m new shares issued at 22 Holdco; £190m raised |

| 19 Nov 2024 | SH01 (£3,100 → £4,100) |

| 27 Feb 2025 | SH01 (£4,100 → £5,100) |

| 25 March 2025 | SH01 (£5,100 → £6,100) |

| FY2024/25 | 179.4m A Ordinary + 110.6m B Ordinary shares issued by 22 Holdco; £450m raised in fresh equity (Clearlake’s share c. £278m); c. £330m on-lent to Chelsea FC |

| May 2025 | 8% of Chelsea FC Women sold to Seven Seven Six (Alexis Ohanian) at $265.2m enterprise valuation |

| 30 June 2025 | Cumulative Clearlake equity in 22 Holdco: £1.794bn (61.85%); cumulative consortium equity: £2.9bn; senior debt £794.2m; PIK £595.9m |

| 12 April 2026 | BlueCo 22 / 22 Holdco accounts for year ended 30 June 2025 filed at Companies House |

| Q1–Q2 2026 | Clearlake doubles GP commitment to Fund VIII to $600m to secure fundraising extension (Bloomberg, Feb 2026) |

| 24 April 2026 | Bloomberg reports investor concern over Eghbali’s “disproportionate” time on Chelsea; Feliciano nears separate $3.9bn personal Padres acquisition |

| 2 May 2026 | Paul Quinn publishes consolidated reconstruction of BlueCo 22 / 22 Holdco capital structure |

Summary table of Clearlake’s total Chelsea-group exposure as of 30 June 2025

| Type | Holder | Counterparty / Issuer | Amount | Maturity | Status |

| Equity (Ordinary A shares) | Blues Investment Midco LP (Cayman, controlled by Clearlake; held for COP III, Fund VII and co-investors) | 22 Holdco Limited | £1.794 billion (cumulative cash contribution; 61.85% of total £2.9bn consortium equity) | Indefinite (10-year sale lock through May 2032) | Active; increased by c. £278m during FY2024/25 |

| Mezzanine / PIK debt (back-leverage) | Clearlake Opportunities Partners III (COP III) | Blues Investment Midco LP | Estimated £300m – £450m principal (not publicly disclosed) | Estimated 2030–2033 | Active; PIK accruing |

| Guarantees / contingent liabilities | None publicly disclosed | – | – | – | – |

| Warrants / options | None publicly disclosed at UK level; possible at Cayman Midco level (typical for COP III deals but not separately verified) | – | – | – | – |

| Other derivatives / structured | None publicly disclosed | – | – | – | – |

| TOTAL Clearlake direct + indirect exposure | c. £2.1 – 2.25 billion (equity + estimated COP III back-leverage) |

By comparison, the third-party debt exposure to the same UK group (i.e. the wider group’s external borrowings) totals £1,390.1m at 30 June 2025 (£794.2m senior + £595.9m Ares PIK), held entirely by JPMorgan/BofA syndicate banks and Ares Management, none of it by Clearlake.

Caveats, gaps and uncertainties in the public record

- Fund-level attribution of the £1.794bn equity is not publicly disclosed. Clearlake’s press release confirms COP III “led” the investment on behalf of “affiliated funds and other partners”, which we read to mean COP III, Clearlake Capital Partners VII (Fund VII), Clearlake co-investment vehicles, and continuation funds. The exact percentage split between these vehicles is private fund information. Markets Group (June 2022) reported Fund VII as a “majority investor” in Chelsea, but Clearlake’s own September 2022 statement frames the lead vehicle as COP III. Both can be true (Fund VII may hold the bulk of the equity ticket, with COP III leading and providing the back-leverage at Midco level and a smaller equity ticket alongside).

- The COP III mezzanine loan to Blues Investment Midco LP is the most economically significant Clearlake-as-lender position, but its principal, pricing, maturity and any equity kickers are NOT in the public record. All figures cited (£300–450m principal; SONIA + 8.5–10.0%; 2030–33 maturity) are reconstructions from PSERS-level reporting, Clearlake’s marketing materials, and Paul Quinn’s analysis (2 May 2026). They should be treated as informed estimates, not audited facts.

- No SEC schedule of investments or Companies House charge filing names a Clearlake fund as a creditor of BlueCo 22, 22 Holdco, BlueCo 22 Midco, BlueCo 22 Properties, or Chelsea FC Holdings. The named creditors in disclosed UK charges (12 July 2022 and 22 August 2023) are the JPMorgan/BofA-led senior syndicate and Ares Management respectively. SEC EDGAR searches return Ares vehicles (ARCC 10-K FY2024; ASIF 10-Q FY2023; CADC schedule) but no Clearlake vehicle disclosing 22 Holdco / BlueCo 22 / Chelsea as a portfolio investment at line-item level.

- Saudi PIF / third-party LP exposure. Saudi Arabia’s Public Investment Fund is reported to be an LP in Clearlake-managed funds (Daily Mail / OneFootball, 2022). PIF’s exposure to Chelsea would therefore be indirect through Clearlake fund LP interests, not direct. No public confirmation of which specific Clearlake funds PIF invests in or in what size has been published.

- PA PSERS is a disclosed COP III LP. PSERS’ public investment reporting confirms that monitoring of COP III’s Chelsea exposure is structured around “downside risk mitigation and credit selection” with sub-advisor CION Ares Management, interesting given that CION/Ares is also the holder of the £595.9m PIK at 22 Holdco, although PSERS’ COP III exposure is structurally separate.

- Bond insurance / surety / NYSE registrations. No publicly searchable NYSE regulatory notice, bond insurance statement, or surety filing was identified covering BlueCo 22 / 22 Holdco / Chelsea FC Holdings debt. The c. $957m senior facility (July 2022) and the £410.2m Ares PIK (September 2023) are private bilateral / club-syndicate facilities, not publicly registered debt securities. The only NYSE-listed entity with disclosed Chelsea exposure is Ares Management Corporation (NYSE: ARES) and its publicly listed BDC Ares Capital Corporation (NASDAQ: ARCC), both Ares-side, not Clearlake-side.

- Fund VIII status (May 2026). Clearlake’s eighth flagship is still in market with target $15bn but reduced size and extended deadline through November 2025 (per Private Equity Wire / Bloomberg Feb 2026); Clearlake doubled its own GP commitment to c. $600m. Fund VIII has no disclosed direct Chelsea exposure as of May 2026.

- Strasbourg, Chelsea Women, and BlueCo 22 Properties exposures. All sit beneath BlueCo 22 Midco / BlueCo 22 Properties and are part of the same consolidated group; Clearlake’s exposure to them is identical in form and proportion to its exposure to Chelsea FC, i.e. 61.85% of the equity of the parent. No separate Clearlake-fund-level instrument has been issued at the level of any sub-subsidiary that is publicly disclosed.

- Movement since 30 June 2025 balance-sheet date. The most recent audited group accounts cover the year to 30 June 2025. Any equity injections, debt drawings or debt repayments between July 2025 and May 2026 will not be reflected in audited Companies House filings until the next annual filing in early 2027. As of May 2026, no public press disclosure reveals additional Clearlake equity injections beyond the £450m in 2024/25, and no announcement has been made of refinancing the £794.2m senior facility maturing July 2027.

- Bloomberg April 2026 reporting notes Chelsea posted a Premier League record £262m pre-tax loss for FY2024/25 at the operating club, and the wider group’s £700.8m loss has prompted some Clearlake LPs to question allocation of management attention. None of this directly affects the size of Clearlake’s exposure but is relevant to its mark-to-market valuation in Clearlake’s quarterly NAV reporting to LPs (which is not public).

In summary, Clearlake’s total Chelsea exposure as a 30 June 2025 reference date is best characterised as c. £1.794 billion of UK-level equity (audited) plus an estimated £300–450m of Cayman-level back-leverage debt (un-audited estimate), for a total exposure on the order of £2.1–2.25 billion, making this Clearlake’s single largest single-asset position outside its enterprise software portfolio and a position concentrated meaningfully in the COP III fund and Fund VII.